Founders' biggest opportunity and toughest competition moment: how to 10x accelerator and achieve rapid scaling

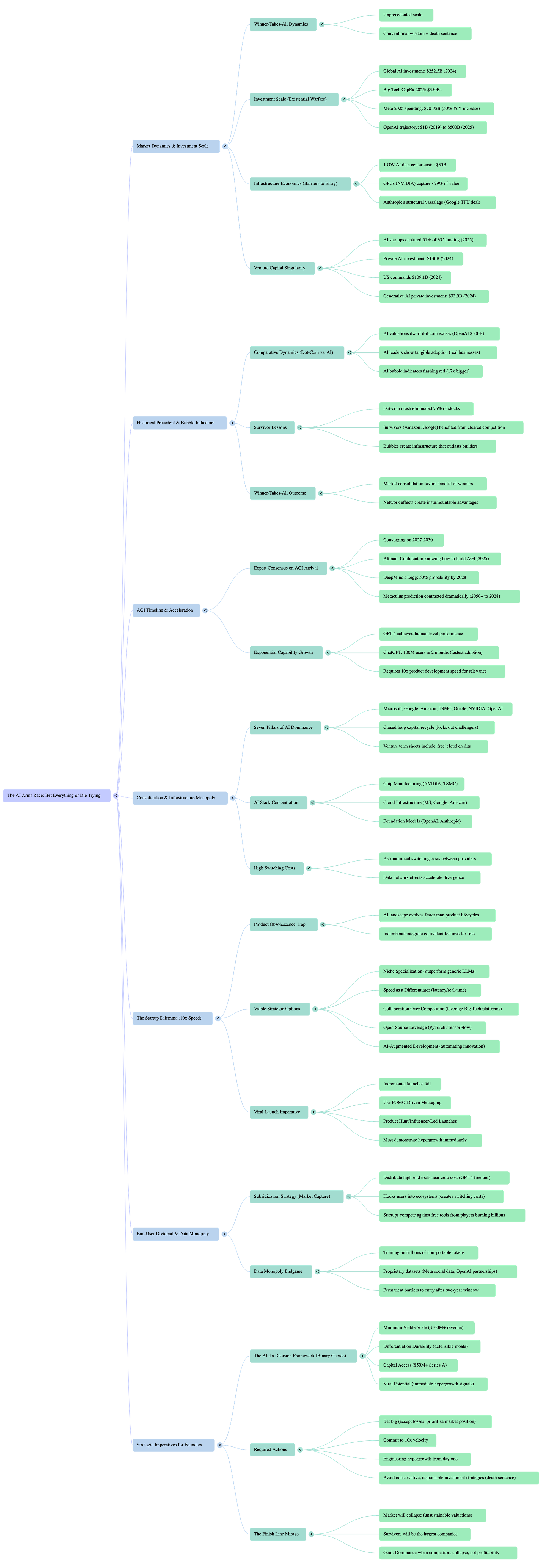

Executive Summary

The AI market has entered a terminal phase where conventional business wisdom becomes a death sentence. With global AI investment reaching $252.3 billion in 2024 and big tech committing over $350 billion in capital expenditure for 2025, the industry is experiencing winner-takes-all dynamics at unprecedented scale. This essay presents a data-driven analysis of the current AI dominance war, its implications for market consolidation, and strategic imperatives for startups operating in an environment where half-measures guarantee extinction.

I. The Mathematics of Survival: Why Normal Investment Equals Death

The Scale of the Arms Race

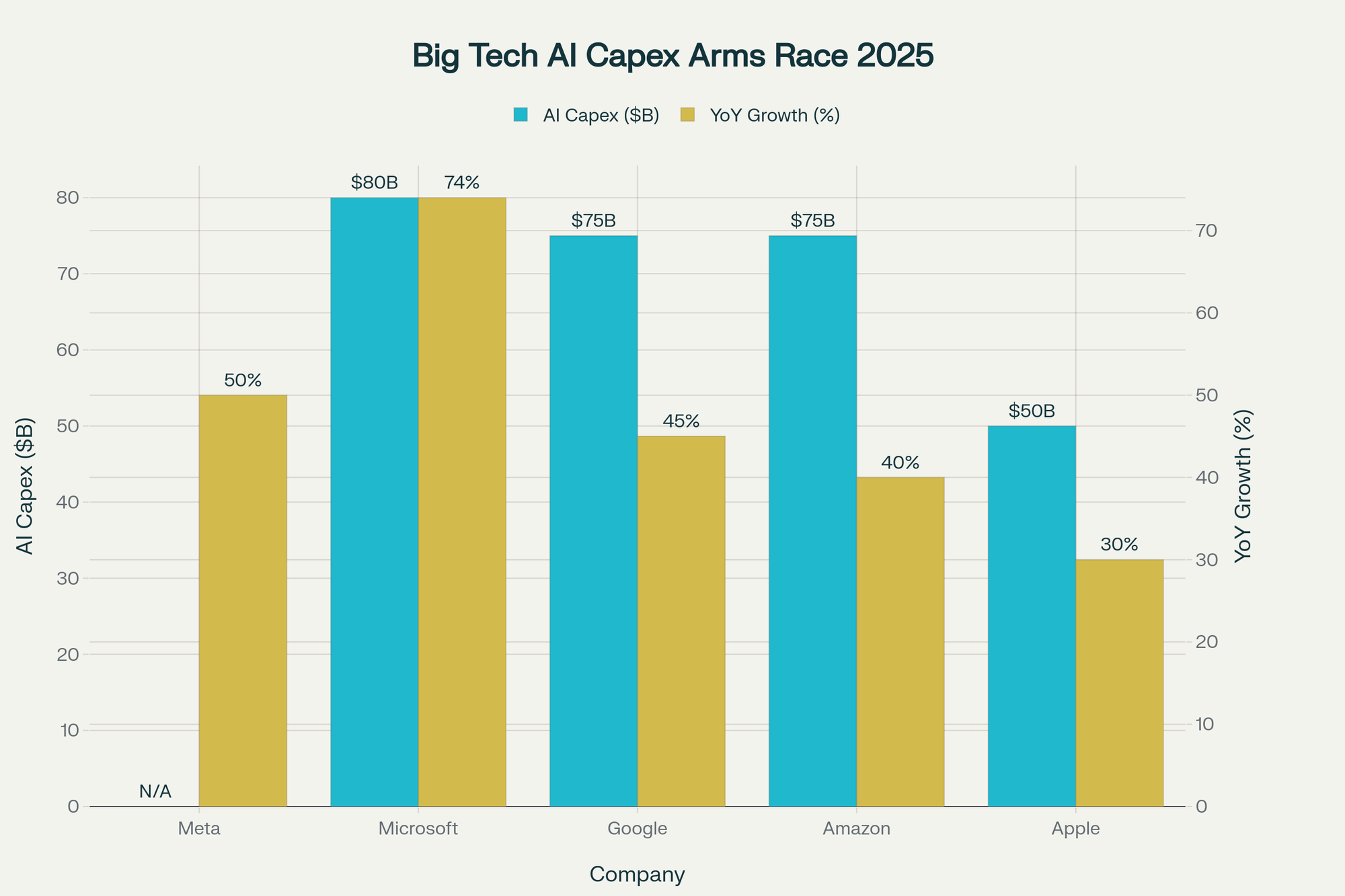

The numbers paint a stark picture. Meta increased its 2025 AI spending guidance to $70-72 billion, a 50% year-over-year increase that triggered an 11% stock plunge as investors questioned returns. Microsoft committed $80 billion with 74% YoY growth. Google and Amazon each allocated approximately $75 billion. This is not incremental investment—this is existential warfare disguised as capital allocation.

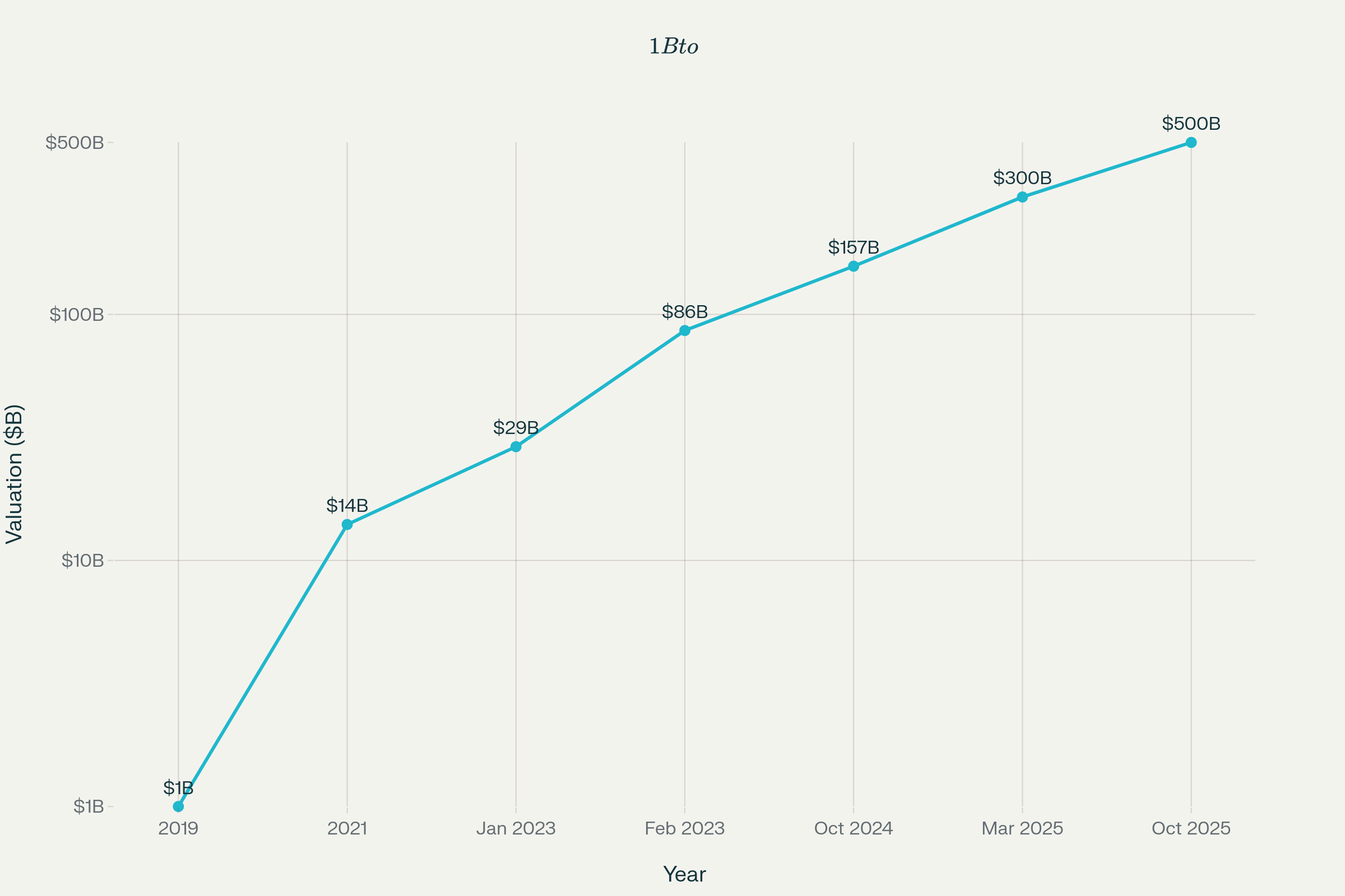

OpenAI's trajectory illustrates the velocity required to survive. The company vaulted from a $1 billion valuation in 2019 to $500 billion by October 2025—a 500x increase in six years. Its annualized revenue hit $13 billion in July 2025, up from $3.7 billion in 2024, yet the company expects to burn $8 billion in 2025 alone and $115 billion through 2029. OpenAI projects it needs $200 billion in revenue by 2030 to achieve cash-flow positivity—requiring 93% annual growth for five consecutive years, a feat almost no company in history has sustained.

Infrastructure Economics: The $35 Billion Entry Fee

The cost structure creates insurmountable barriers. Building one gigawatt of AI data center capacity costs approximately $35 billion, with GPUs alone accounting for $13.65 billion (39% of total capex). A single GB200/NVL72 rack costs $5.9 million—$3.4 million for compute hardware and $2.5 million for physical infrastructure. NVIDIA's gross profit dollars represent roughly 29% of all AI data center spending, meaning the company captures nearly one-third of industry infrastructure value.

Anthropic's recent commitment to purchase up to 1 million TPUs from Google in a deal "worth tens of billions of dollars" demonstrates the scale of dependency. This represents 10-16% of Anthropic's entire $183 billion valuation locked into a single infrastructure provider—Google, which simultaneously owns 10% of Anthropic's equity and competes directly through Gemini. This is not partnership; it is structural vassalage where the infrastructure provider profits whether the AI company succeeds or fails.

The Venture Capital Singularity

AI startups captured 51% of all venture funding between January and October 2025, with private AI investment reaching $130 billion in 2024—a 40.38% increase year-over-year. In 2025, AI-related investments accounted for 51% of total VC deal value versus just 12% in 2017. The U.S. alone commanded $109.1 billion in private AI investment in 2024—nearly 12 times China's $9.3 billion and 24 times the U.K.'s $4.5 billion.

Generative AI private investment reached $33.9 billion in 2024, up 18.7% from 2023 and 8.5 times higher than 2022 levels. This represents more than 20% of all AI-related private investment. The funding concentration creates a binary outcome: either you capture massive capital and join the race, or you are irrelevant.

II. Historical Precedent: Lessons from the Dot-Com Bubble

Comparative Dynamics: 2000 vs 2025

The parallels to the dot-com bubble are undeniable yet incomplete. The Nasdaq peaked at 5,048 in March 2000 with a forward P/E ratio of 60x before crashing 78% by October 2002. Today's Nasdaq sits around 16,000 with a forward P/E of 26x—elevated but not stratospheric. However, AI companies command valuations that dwarf dot-com era excess. OpenAI at $500 billion exceeds Chevron ($294B), Samsung ($263B), and Salesforce ($257B) despite projecting $44 billion in cumulative losses through 2028.

The critical difference: many dot-com companies had zero revenue and no path to profitability. Today's AI leaders show tangible adoption—78% of companies reported using AI in 2024, up from 55% in 2023. OpenAI generates $13 billion in annualized revenue with 500 million weekly active users and 20 million paid subscribers. Anthropic's annual revenue run rate approaches $7 billion. These are real businesses, not vaporware.

Yet the bubble indicators are flashing red. An analyst noted the AI bubble is "17 times bigger than the dot-com bust" based on market capitalization concentration. AI assets see 54% of investors viewing them as a bubble. The top three companies (NVIDIA, Microsoft, Apple) comprise approximately 40% of S&P Tech market cap versus 25-30% for Cisco, Intel, and Microsoft at the 2000 peak.

Survivors and Casualties: The Winner-Takes-All Outcome

The dot-com crash eliminated 75% of tech stocks, but survivors like Amazon, eBay, and Google became the foundation of the modern internet economy. Amazon's stock fell 90% from $107 to $7 but recovered to dominate e-commerce by opening its platform to third-party sellers and building AWS. Google IPO'd in 2004 after the crash, benefiting from cleared competition and cheap infrastructure (fiber-optic cables, server farms) left behind by failed companies.

The pattern is clear: bubbles create infrastructure that outlasts the companies that build it. The dot-com boom left behind fiber-optic cables, data centers, and a venture capital ecosystem that enabled the next generation. The current AI boom is constructing GPU clusters, training infrastructure, and foundation models that will persist regardless of which companies survive.

The strategic implication: being among the last companies standing when the bubble bursts is the only objective that matters. Market consolidation favors a handful of winners who capture the entire value chain. Platform markets exhibit "winner-takes-all" or "winner-takes-most" dynamics where network effects and economies of scale create insurmountable advantages for leaders.

III. The AGI Timeline: Racing Toward the Singularity

Expert Consensus on AGI Arrival

Leading AI researchers converge on AGI (Artificial General Intelligence) emerging between 2027 and 2030. Sam Altman stated in early 2025 that "we are now confident we know how to build AGI as we have traditionally understood it," predicting functional AGI precursors could join the workforce imminently. OpenAI established a Superalignment team in 2023 with a four-year timeline, tacitly acknowledging they expect to create AGI by 2027.

Shane Legg, DeepMind's Chief AGI Scientist, has maintained since 2010 a 50% probability of AGI by 2028—a prediction he reiterated in 2023. Demis Hassabis suggested AGI is "roughly 3-5 years away" in late 2023, placing his estimate in the late 2020s. Yoshua Bengio forecasts 2029 with 72% confidence.

The Metaculus forecasting community's timeline has contracted dramatically. In 2018-2019, the mean forecast for AGI was 2050 or later—30-50 years away. By late 2023, the collective prediction had shrunk to approximately 2028-2029, representing a reduction from 80 years to 5 years as major AI milestones (GPT-3, ChatGPT, GPT-4) occurred.

The Exponential Acceleration

The timeline compression reflects exponential capability growth. GPT-3 (2020) demonstrated unprecedented natural language processing. GPT-4 (2023) achieved human-level performance on professional exams. ChatGPT reached 100 million users in two months—the fastest adoption of any technology in history. Each breakthrough shortened expectations by years or decades.

This acceleration creates a strategic paradox for startups: you are building today for a market that will be fundamentally different tomorrow, but when tomorrow arrives, your "visionary" product is already obsolete. The product development cycle must operate at 10x speed merely to stay relevant, yet most startups lack the resources to sustain this velocity.

IV. Market Consolidation and Infrastructure Monopoly

The Seven Pillars of AI Dominance

Seven firms—Microsoft, Google, Amazon, TSMC, Oracle, NVIDIA, and OpenAI—now own the infrastructure of the AI era. They invest in one another, sit on each other's boards, and recycle capital in a closed loop that locks out challengers. Microsoft funds OpenAI, then bills it for Azure compute. Google and Amazon both bankroll Anthropic while competing for its workloads. NVIDIA sells GPUs to everyone, then invests in those buyers.

This circular ownership creates structural monopoly. One European bank delayed its internal AI rollout by three months because available GPUs were tied to a specific cloud provider's credit package. Venture term sheets increasingly include "free" cloud credits that must be spent on the investor's platform—dollars that never leave the system.

The AI stack exhibits powerful concentration dynamics across four layers: (1) chip manufacturing (NVIDIA, TSMC), (2) cloud infrastructure (Microsoft, Google, Amazon), (3) foundation models (OpenAI, Anthropic, DeepMind), and (4) application layer. Control over foundational layers grants disproportionate power over the entire value chain. It is "virtually impossible for a startup to build, deploy, and distribute an AI product without relying, at least in part, on resources provided by Big Tech".

Platform Wars and Network Effects

Platform markets historically yield winner-takes-all outcomes where a single platform captures significantly more than 50% of market share. Network effects create increasing returns to scale: the more users join a platform, the more valuable it becomes, attracting more users in a self-reinforcing cycle. Early movers establish leads that become nearly impossible to overcome.

Research shows that where multi-homing costs (the ability to use multiple platforms simultaneously) are high, a single platform is more likely to dominate. In AI infrastructure, switching costs are astronomical—migrating to alternative providers requires rewriting entire technology stacks, retraining models on different hardware architectures, and renegotiating supplier relationships.

The AI market exhibits even stronger consolidation forces than previous platform wars. Data network effects mean companies with more data train better models, which attract more users, generating more data—a flywheel that accelerates divergence between leaders and followers. Meta's 15 years of social interaction data and OpenAI's exclusive publisher partnerships create proprietary datasets that cannot be replicated.

V. The Startup Dilemma: 10x Speed with 1x Resources

The Product Obsolescence Trap

Startups face an impossible calculus. Building a product today requires 12-18 month development cycles, yet the AI landscape evolves faster than product lifecycles. By the time you launch your "next-generation" solution, the foundation models you built on have been superseded twice, your competition has raised $500 million, and incumbents have integrated equivalent features into their platforms for free.

AI-driven enterprises can accelerate product development through automation, reducing Innovation Product Development Debt (IPDD) and bringing products to market faster than traditional startups. Case studies show AI tools completing innovation analysis in 4 weeks versus 16-20 weeks manually, achieving 75% accuracy in classifying consumer needs, and predicting expert ratings 23% more accurately than crowd assessments.

Yet this advantage is accessible to everyone, not just startups. Big tech companies leverage the same AI tools at greater scale with vastly more resources. The "democratization" of AI technology paradoxically increases competitive intensity rather than leveling the playing field.

Strategic Options for Startups

Research identifies five viable strategies for startups competing against AI giants:

1. Niche Specialization: Focus on specific use cases where generic models fail. Specialized AI models for accounting, healthcare, or legal applications can outperform general-purpose LLMs in accuracy, latency, and hallucination rates. Startups excel by serving underserved segments that tech giants deprioritize.

2. Speed as a Differentiator: Optimize for latency and real-time processing. Generic models suffer from response time delays that specialized, streamlined systems can eliminate. Speed transforms user experience and creates competitive moats in time-sensitive applications.

3. Collaboration Over Competition: Rather than competing directly, leverage big tech platforms (Google's TensorFlow, Amazon's AWS ML services) to reduce development costs while innovating in areas giants don't prioritize. Partner strategically rather than fighting impossible battles.

4. Open-Source Leverage: Utilize TensorFlow, PyTorch, and OpenAI's open models to build sophisticated AI capabilities without massive R&D investments. Open-source frameworks democratize access to cutting-edge technology.

5. AI-Augmented Development: Use AI to automate the means of innovation, freeing human founders to focus on strategic ends. This slashes time and cost for building products, enabling leaner operations that scale revenue without proportional expense increases.

The Viral Launch Imperative

The quality of rapid iteration decreases as speed increases, yet startups have no choice but to run at 10x velocity. Attention is fragmented across thousands of products, creating extraordinarily high barriers to visibility. To join the big game requires a big jump at launch—the right product solving the right pain for the right ICP (Ideal Customer Profile), combined with virality mechanisms that demonstrate hypergrowth immediately.

Viral product launch strategies include:

- Influencer-Led Launches: Partner with micro-influencers (10k-100k followers) with high engagement rates. Their authentic endorsements convert better than macro-influencers with passive audiences.

- Product Hunt Launches: Leverage the Product Hunt community for tech-enabled products. Successful launches require preparation, timing (Tuesday-Thursday, 12:01 AM PST), and active engagement with every comment.

- FOMO-Driven Messaging: Use scarcity and urgency ("Only 500 made," "Gone in 3 minutes") to trigger immediate action. Time-sensitive framing activates fear of missing out, forcing rapid purchase decisions.

- Event-Based Launches: Concentrate promotional energy into high-impact moments (Apple-style virtual events) that create massive attention spikes and media coverage.

The pattern is clear: incremental launches fail. Only breakthrough, viral-scale launches that demonstrate immediate traction secure follow-on funding and resources to sustain 10x development velocity.

VI. The End-User Dividend: Free Tools and Market Control

The Subsidization Strategy

End users benefit enormously from the AI arms race. Big players distribute high-end tools at near-zero marginal cost to accumulate market share and user data. ChatGPT offers GPT-4 capabilities in free tiers. Meta releases Llama models as open source. Google integrates Gemini across its product suite at no additional charge. Microsoft bundles Copilot into Office 365 subscriptions.

This is not altruism—it is market capture strategy. Free or cheap access hooks users into ecosystems, generating data network effects and creating switching costs. Once users build workflows around ChatGPT or integrate Gemini into business processes, migration becomes prohibitively expensive regardless of superior alternatives.

The subsidization creates a perverse dynamic: startups must compete against free or near-free tools from companies willing to lose billions annually. OpenAI projects $44 billion in cumulative losses through 2028. Anthropic burns billions on infrastructure commitments. These losses are strategic investments in market control, not business failures.

The Data Monopoly Endgame

AI companies are consolidating vast data monopolies by training models on trillions of tokens from diverse sources. These datasets are non-portable—inextricably linked to expensive training runs costing $100 million and spanning months. Meta's 15 years of social interaction data and OpenAI's exclusive publisher partnerships create proprietary advantages that cannot be replicated.

Data network effects entrench monopolistic positions. Companies with more data train better models, attracting more users, generating more data in a self-reinforcing cycle. This creates permanent barriers to entry beyond an approximately two-year window, after which data set monopolies become "permanent fixtures".

VII. Strategic Imperatives for Founders

The All-In Decision Framework

Founders face a binary choice: commit fully to the AI race or exit the battlefield entirely. Partial commitment guarantees failure. The decision framework requires assessing:

1. Minimum Viable Scale: Can you achieve venture-scale outcomes ($100M+ revenue) in your niche? If not, the investment required to compete exceeds potential returns.

2. Differentiation Durability: Does your specialization create defensible moats against both startups and big tech integration? Specialized models, proprietary data, or unique distribution channels provide temporary protection.

3. Capital Access: Can you raise $50M+ in Series A to fund 18-24 months of 10x-speed development? Undercapitalized startups cannot sustain the velocity required to stay relevant.

4. Viral Potential: Does your product/market fit enable viral distribution at launch? Without immediate hypergrowth signals, you cannot attract follow-on funding to compete long-term.

If the answer to any question is "no," conventional business wisdom suggests pivoting to non-AI markets or becoming an acquisition target for companies that can integrate your technology into broader platforms.

The CrossLike Approach: Enabling Viral Velocity

At CrossLike, we focus on enabling founders to make their products and launches viral at the most critical moment when they need to demonstrate rapid scaling. The thesis is simple: in an era where normal growth rates equal death, the only viable strategy is engineering hypergrowth from day one.

This requires:

- Strategic Launch Timing: Coordinating product readiness with market momentum, narrative fit, and attention windows.

- Virality Mechanisms: Building FOMO, social proof, and network effects directly into product architecture and go-to-market execution.

- Rapid Iteration Infrastructure: Leveraging AI tools to compress product development cycles from 12 months to 12 weeks without sacrificing quality.

- Data-Driven Amplification: Using real-time analytics to identify and double down on early traction signals, multiplying initial momentum.

The goal is not incremental improvement—it is creating the "big jump" that signals to investors, customers, and the market that your startup belongs in the race.

VIII. Conclusion: The Finish Line Mirage

The Bubble's Inevitable Conclusion

The AI market will collapse. Not because the technology fails, but because current valuations and investment rates are unsustainable. OpenAI cannot grow revenue at 93% annually for five consecutive years. The combined $350+ billion in annual big tech capex cannot generate proportional returns. At some point, investor patience exhausts, capital dries up, and the market corrects violently.

History provides the template. The dot-com crash eliminated 75% of companies but left behind infrastructure, talent, and cleared markets that enabled Amazon, Google, and the modern internet. The AI bubble will follow the same pattern: mass extinction of undercapitalized players, consolidation around 3-5 dominant platforms, and a decade of infrastructure utilization by the survivors.

Crossing the Finish Line Bloodied but Alive

The strategic imperative is clear: be among the largest companies when the bubble bursts. Size matters not for efficiency but for survival. Companies with the most capital reserves, largest user bases, and deepest infrastructure commitments will weather the correction. Everyone else becomes acquisition targets or failures.

This means accepting losses, burning capital at rates that would be reckless in normal markets, and prioritizing market position over profitability. It means recognizing that conservative, "responsible" investment strategies are death sentences in winner-takes-all markets. It means understanding that the finish line is not profitability—it is dominance when competitors collapse.

Final Calculus for Founders

We live in the era of accessible high-end technology and hyper-competitive 10x-evolving markets. The paradox is complete: the same tools that democratize access also intensify competition to existential levels. Free AI tools enable anyone to build; therefore, building alone is insufficient. You must build faster, launch bigger, and scale more aggressively than ever before.

The choice is stark:

- Bet big: Raise massive capital, commit to 10x velocity, engineer viral growth, and fight for a position among the survivors. Accept that you will probably fail, but if you succeed, you dominate.

- Bet small: Operate conservatively, grow steadily, manage resources responsibly—and guarantee irrelevance as better-funded competitors bury you.

- Don't bet: Exit the AI arms race entirely, focus on non-AI markets, or position for acquisition before the bubble bursts.

There is no middle path. The AI market punishes hesitation and rewards audacity. The companies that cross the finish line will be bloodied, burning billions, and barely solvent—but they will be the only companies that matter. Everyone else will be forgotten.

The race is on. Choose your speed accordingly.

About CrossLike: We enable founders to make their product launches viral at critical moments when demonstrating rapid scaling determines survival. In an era where normal growth equals death, we engineer hypergrowth from day one.

Mind map of the article